31

October 2025

Online Funds’ performance for the quarter ended 30 September 2025

Adriaan Pask

Chief Investment Officer,PSG Wealth

Domestic online funds performance and positioning

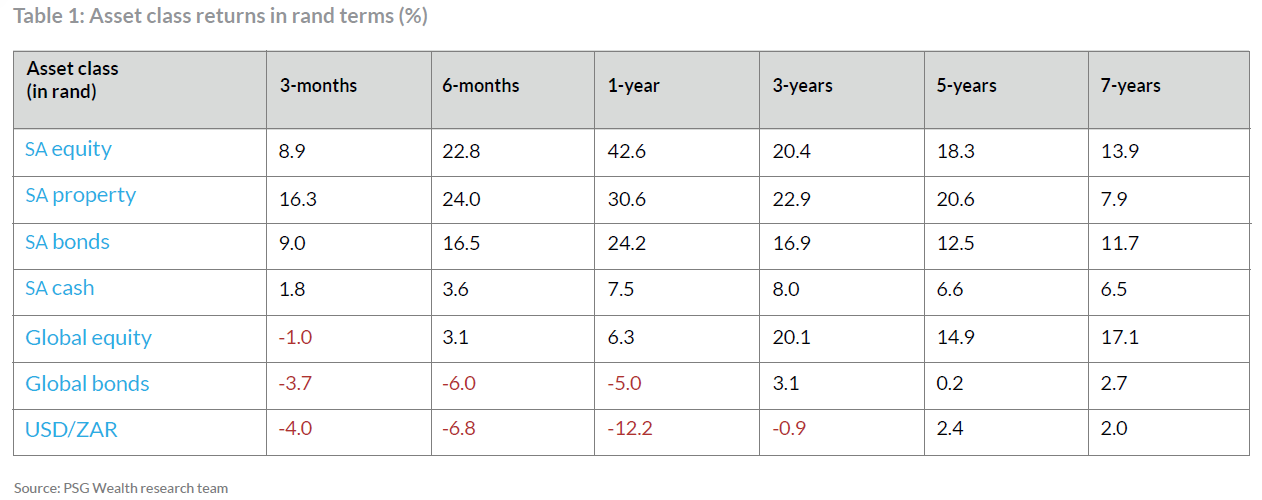

South African equities delivered an impressive 6.50% return in September, capping off the JSE’s best quarter this year with a 9.70% return. This brings the index’s year-to-date gain to more than 30%. The primary drivers of this performance were precious metal miners, with platinum miners surging 46% month-on-month and gold miners rising 27% over the same period. Together, these sectors accounted for most of the JSE’s performance in September and are now responsible for two-thirds of the JSE’s gains in 2025. Investment conglomerates Naspers and Prosus also made significant positive contributions, benefiting from the strong momentum in Chinese equities, particularly their largest underlying investment, Tencent, which rose 11% month-on-month and 60% year-to-date.

Global equity markets delivered solid returns in the third quarter and year-to-date, with US equities reaching record highs. Trade tensions eased during the quarter whilst corporate earnings remained resilient. The US Federal Reserve cut interest rates by 25 basis points in September, responding to weaker labour market data, with other central banks following suit. Emerging markets outperformed developed markets, with the MSCI EM Index returning 7.20% month-on-month and 28% year-to-date, versus the MSCI World Index’s 3.30% monthly and 17.90% year-to-date returns. Chinese equities, particularly offshore listings, drove emerging market performance. In developed markets, mega-cap technology stocks led gains, though returns remained concentrated, with six of eleven S&P 500 sectors delivering single-digit year-to-date returns despite the index’s 15% year-to-date performance.

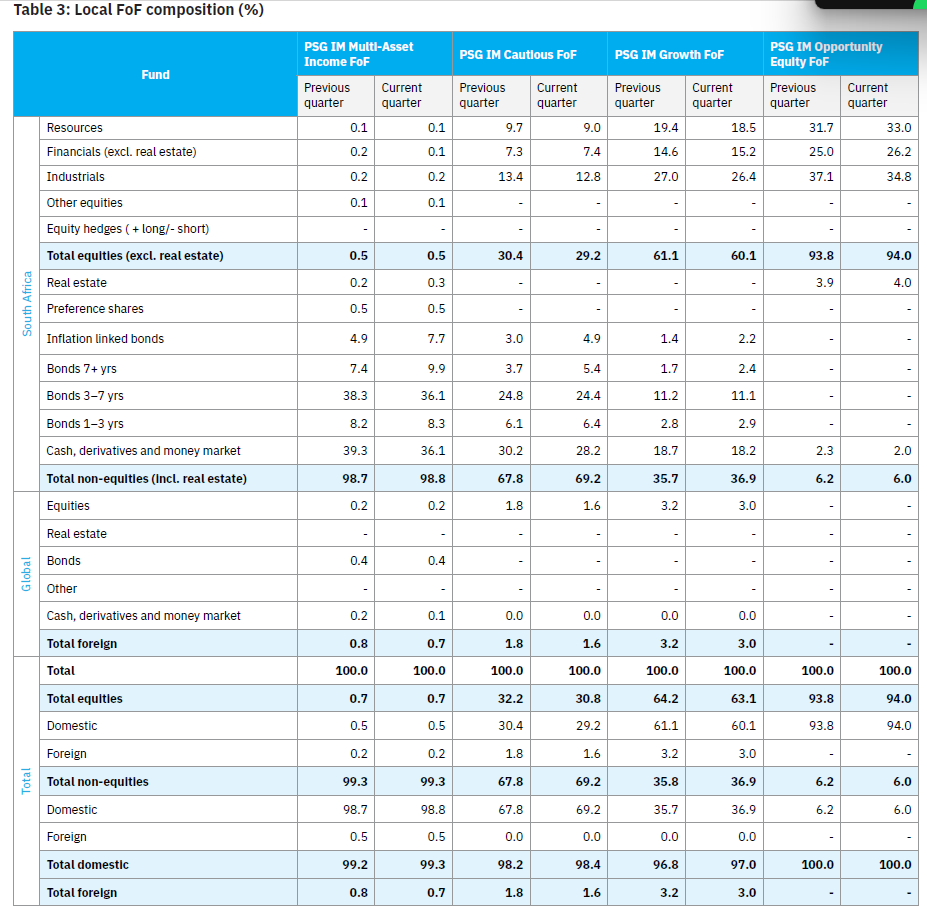

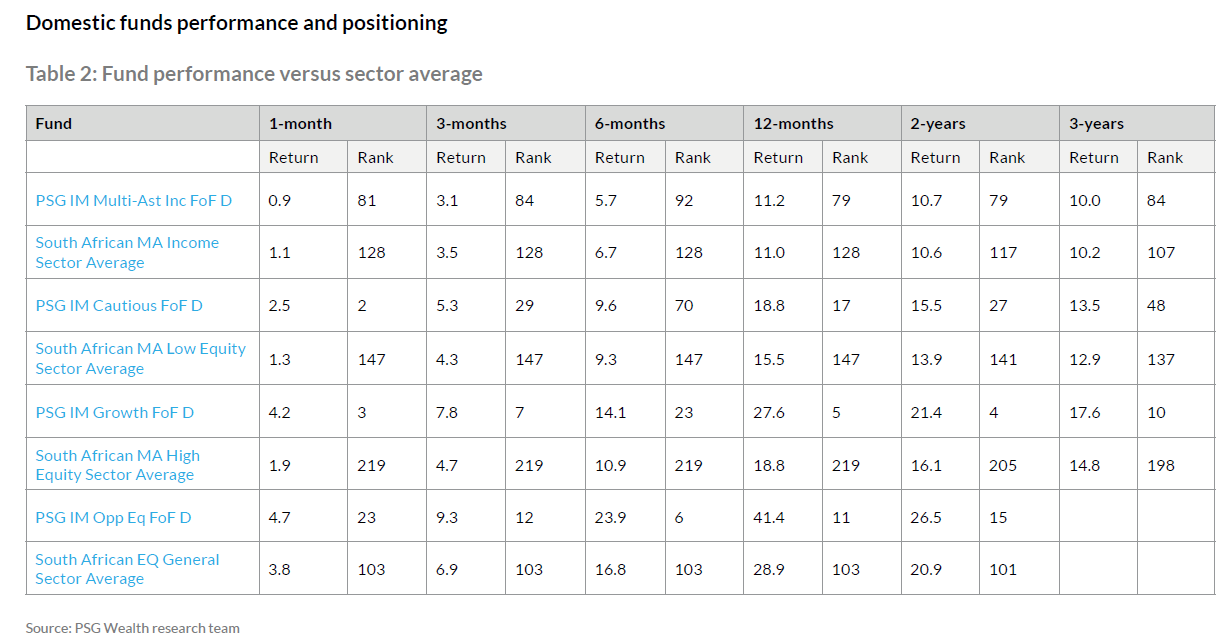

The multi-asset solutions delivered positive absolute returns during the quarter, with all building blocks contributing to performance. Within the equity building block, security selection in resources was the primary performance driver. AngloGold Ashanti, Northam Platinum and Gold Fields were amongst the top contributors, whilst WBHO, Foschini and Super Group moderated gains. The income building blocks also generated positive absolute returns, with government bonds providing stability and driving performance throughout the quarter. Our underlying managers maintain a preference for the belly of the yield curve, where valuations remain relatively attractive. The income building block also includes corporate bonds, with our underlying managers favouring bank issuances.

Throughout the quarter, our underlying managers made tactical asset allocation adjustments in response to evolving market conditions. Within equities, resources sector exposure was reduced, resulting in lower allocations in the Cautious and Growth Funds of Funds, with the Growth FoF experiencing the larger reduction of 1.50%. Financial and real estate sector allocations were similarly reduced across both funds. These reductions were reallocated to South African fixed income, specifically the belly of the yield curve, where investors can capture attractive yields without assuming equity risk. Within domestic fixed income, our underlying managers implemented maturity-specific adjustments, reducing exposure to longer-dated bonds (exceeding seven years) whilst significantly increasing allocations to the three-to-seven-year maturity segment. This resulted in allocation increases of 8.10% and 4.70% to this segment in the Income and Cautious Funds of Funds respectively. Exposures to one-to-three-year bonds and cash positions were also reduced as capital was redeployed towards more compelling risk-adjusted opportunities.

Internationally, global equity allocations within the Cautious and Growth Funds of Funds increased by 1.80% and 3.40% respectively, reflecting our underlying managers’ constructive outlook for international equities. These allocation adjustments demonstrate a proactive approach to portfolio construction and risk management, dynamically adjusting exposures to optimally position the funds within the prevailing investment landscape.

The PSG IM Opportunity Equity Fund of Funds returned 6.50% for the month, outperforming its benchmark by 2% and extending year-to-date alpha to 8.80%. Performance benefitted from our underlying managers’ exposure to platinum and gold miners, as well as holdings in Naspers and Prosus. The solution remains fully invested in domestic growth assets. Our underlying managers marginally reduced industrial sector allocations in favour of domestic cash. The fund’s composition remained unchanged during the quarter.