31

July 2025

Online Funds’ performance for the quarter ended 30 June 2025

Adriaan Pask

Chief Investment Officer,PSG Wealth

Domestic online funds performance and positioning

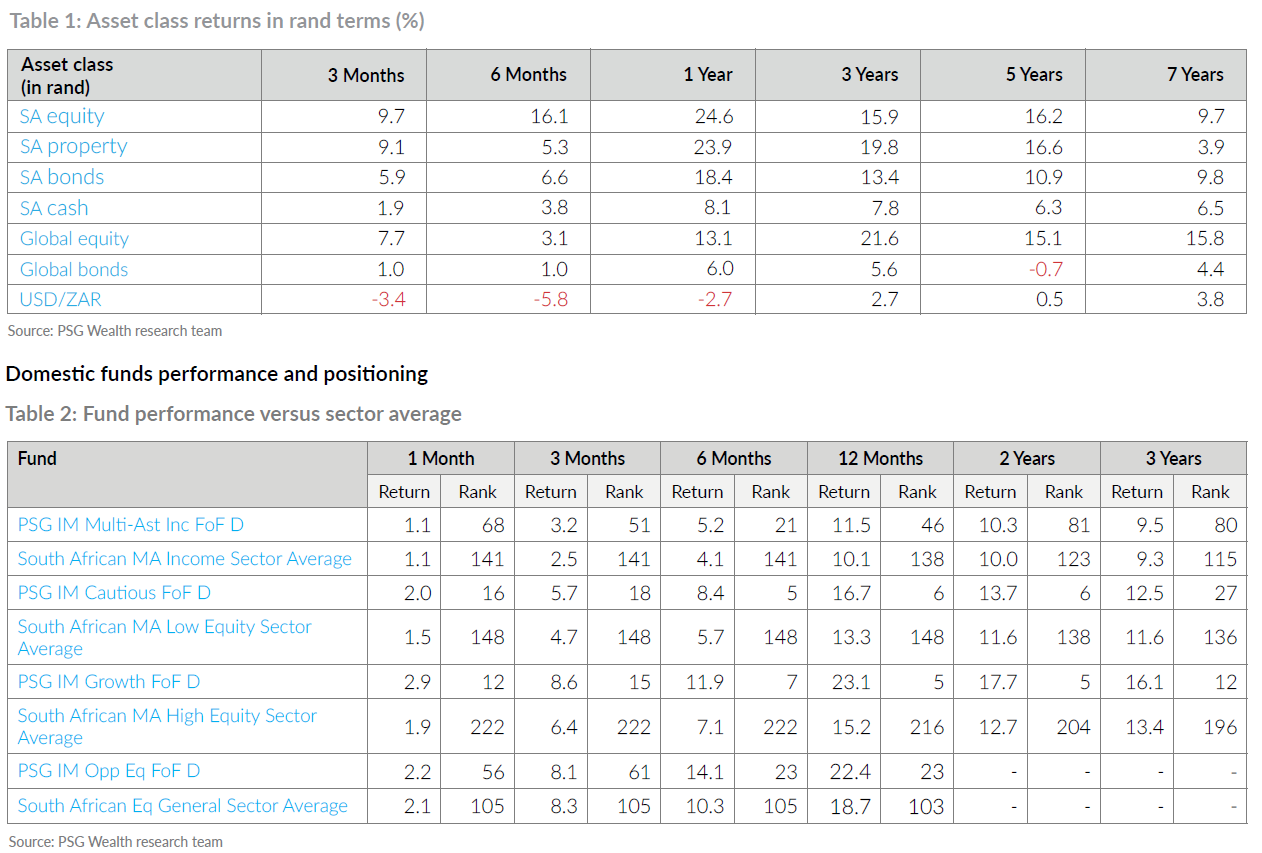

South African equities delivered a 10% return over the past three months and more than 16% year-to-date (YTD). Growth was driven by strong gains in the resources sector, up nearly 40% YTD, alongside steady gains from industrials, up by 17% YTD. Although financials delivered positive returns, they underperformed the broader market and the top-performing sectors. The sector registered a 7.80% gain over the last three months and a modest 6% YTD. Listed property delivered a 9% return over the quarter, bringing its YTD return to 5.30%. Local fixed-income assets also enjoyed a strong quarter across most bond maturity segments, contributing to an overall positive performance for the year. The All Bond Index (ALBI), which represents the broader domestic bond market, delivered a 5.90% return over the past three months.

Global equity markets rebounded in the second quarter, largely recovering from the uncertain start to the year. International developed markets, particularly in Europe and Asia (with notable gains in the Hang Seng Index), delivered a significant YTD performance, while the US market demonstrated strong quarterly recovery. Despite April’s volatility brought on by tariff uncertainties, US equities bounced back strongly, with robust earnings reports, particularly from the technology sector, driving much of the recovery.

The multi-asset solutions added alpha this past quarter. The equity building block drove portfolio returns as security selection within the resources and industrials portions added value, with Northam and AngloGold Ashanti being the top contributors from the resources allocation. Other notable contributors to returns included Adcorp, Telkom and Naspers. The income-generating portion of the portfolios provided stability throughout the quarter, as government and corporate bonds favoured by our underlying managers added value.

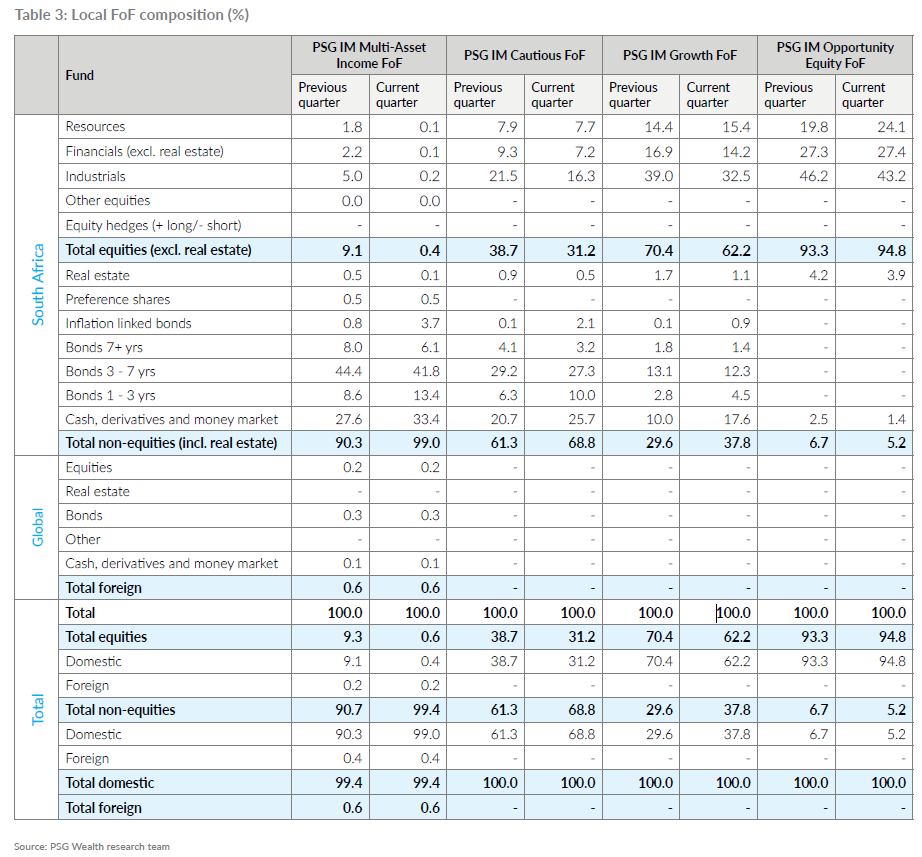

All three PSG IM multi-asset funds—the Multi-Asset Income FoF, Cautious FoF, and Growth FoF— were de-risked towards the end of the quarter through the inclusion of the PSG Enhanced Interest Fund, which will serve as the local cash building block. To fund this addition, we realised profits from our equity building block. This resulted in an increased allocation to fixed-interest assets across these funds. Specifically, in the PSG IM Multi-Asset Income FoF, we rotated the equities allocation into the PSG Enhanced Interest Fund. At an asset allocation level, this translated to a higher weighting in cash, aligning with the fund’s goals of income generation and capital preservation.

Similarly, the PSG IM Cautious FoF saw an increase in liquidity; we reduced our equity allocation by 10 percentage points and moved those proceeds into the cash building block. The same was done in the Growth FoF, trimming exposure by 10 percentage points and allocating the proceeds to the cash building block. While this portfolio activity suggests a defensive posture in the short term, we believe the current market environment is setting the stage for us to access growth opportunities at more attractive entry points.

The PSG IM Opportunity Equity FoF returned 8.10% over the quarter, narrowly trailing its benchmark by 0.20%. However, the fund maintains its lead YTD, outperforming its benchmark by 4%. This solution remains fully invested in domestic growth assets, with equity allocation increasing quarteron- quarter. This shift occurred as our underlying managers reduced their exposure to listed property and cash, favouring an increased allocation to resources. No changes were made to the fund’s composition during the quarter.

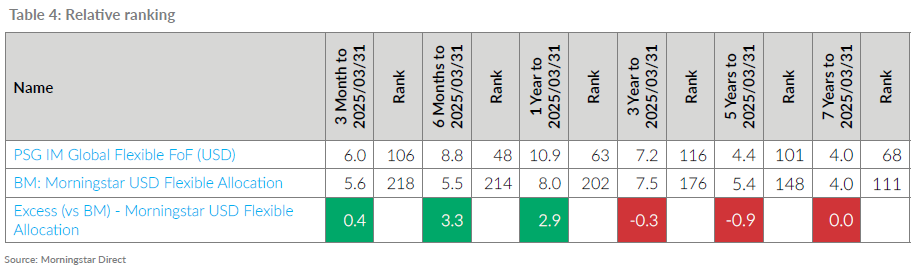

PSG IM Global Flexible Fund of Funds (FoF)

The Global Flexible FoF delivered a 6% return over the quarter, exceeding its benchmark by 0.40%. This positive momentum contributed to an impressive YTD return of 8.80%, maintaining a significant 3.30% lead over the benchmark. Over the past 12 months, the fund has returned 10.90%, comfortably ahead of the benchmark’s 8%. A key driver of YTD returns was PSG Global Flexible, which achieved a 23% return over six months. Other notable performers included Baillie Gifford Managed, with a 13.10% gain over three months and 13.50% over six months, and HSBC Global Strategy Dynamic, which rose by 10.50% over three months and 10.40% over six months.

Muting gains were Ninety One Global Macro Allocation and Sarasin, which lagged behind their sector peers over the past six months. The most significant drag on performance came from Veritas Global Real Return, which posted negative returns of -3% over three months and -3.50% over six months. The latter’s underperformance stemmed from security selection in healthcare and industrials, an underweight position in the tech sector and the use of index futures. Overall, the fund of funds’ composition remained consistent, with no changes made over the quarter.